TaxMe provides the most simple, secure, powerful and efficient method for electronic filing in the market.

Simple: With TaxMe you don't need to register an ONLINE ACCOUNT, you don't need USERNAMES or PASSWORDS or IRS PIN's. TaxMe's approach is simpler and more efficient than all our competitors. All our competitors require you to create an online account before e-filing a return which can take valuable time to complete. With us, your return can be completed in a matter of minutes and IRS acknowledgments can be generated in less than two hours.

Secure: Most web portals provide a method for customers to access account information via setting up an ONLINE ACCOUNT, by creating USERNAMES and PASSWORDS. This method opens an avenue for accessing your information over the internet and potentially exposing your data for attacks. TaxMe developed a face recognition utility to keep your data secure and eliminate repetitive tasks. All server-client communications meet general standards of cryptographic protocols designed to provide communication security over the internet.

Powerful: TaxMe develops its own software, uses its own platform to originate your returns and transmits the data to the Internal Revenue Service (IRS), Social Security Administration (SSA) and / or state agencies. TaxMe is an authorized IRS e-file provider classified as an Electronic Return Originator(ERO), Software Developer and a Transmitter. See for yourself 😉.

TaxMe has all proprietary rights to all electronic filing software which allows us to avoid system interruptions and down times and gives us competitive advantage to customize our products. We can easily apply the latest designs, architectures and technologies and configure them based on direct feedback from our customers or by improving inefficient processes. We control the entire transmission cycle from the time the data is submitted online through the acknowledgment phase. TaxMe does not use or rely on third party software as the majority of our competitors do.

Efficient: We use a 5 digit Self-Select PIN (Personal Identification Number) Method for Modernized e-File (MeF). It is the most efficient option for taxpayers to use when signing their electronic forms. The PIN number is a non-universal number, therefore, taxpayers can choose a different number every time they file a return. Taxpayers may choose any 5 digit number except all zeros.

TaxMe is an IRS approved ERO, Software Developer and Transmitter. These three categories allows us to offer the most convenient way to sign an employment tax return. Below are four options to electronically sign an employment tax return:

Form 8879-EMP Practitioner PIN Signature method: TaxMe uses this method. It can only be used if the taxpayer uses an ERO. Taxpayer chooses a five-digit, self-selected PIN as their signature. Taxpayer can authorize the ERO to input this number in the software or must input physically directly into the software. The PIN number cannot be all zeros. Form 8879-EMP must be completed by the ERO and must be retained by both the ERO and the taxpayer for 3 years from the return due date. If a paid preparer is involved, the ERO is responsible to include the required information in the return. The paid preparer should also keep a copy of the return approved and signed by the taxpayer. Form 8879-EMP should not be mailed to the IRS unless the IRS requests a copy.

Scanned Form 8453 Signature method: It involves signing a peper Form 8453-EMP and attaching it electronically to the e-filed return as a PDF document. This document is a jurat, it has the same legal effect as if the taxpayer had actually and physically signed the return. This form can authorize an ERO, a Transmitter or an ISP to send the return to the IRS. The form must be retained by the taxpayer and should not be mailed to the IRS.

Form 8655 Reporting Agent PIN Signature method: A reporting agent is an accounting service, franshiser, bank or other entity authorized to prepare, sign and electronically file employment forms for taxpayers. Reporting agents sign all electronic returns they file with a 5-digit PIN signature. The reporting agent PIN is issued through the IRS e-file application process. Reporting agents can transmit returns directly or use a third-party Tranmitter. Reporting agents must submit Form 8655 to the IRS prior to updating or submitting an IRS e-file application. Form 8655 gives the tax professional authority to sign the client's return with their reporting agent's 5-digit PIN.

Online Signature PIN method (10-digit IRS PIN): This method is available for an authorized individual to act for an entity in legal and/or tax matters and is held liable for filing all 94x returns and making all 94x tax deposits and payments. It authorizes an entity to file no more than 5 returns per year. This method does not give authorization to file bulk returns or returns for other businesses. To become an Online e-Filer, the applicant must first complete the 94x PIN Registration Process using commercial software. Registration can take up to 45 days to process. The PIN assigned to the participant consists of a 10-digit number which is used to electronically sign an employment tax return.

Click each link to view the different forms supported under each category.

Forms 940: Employer's Annual Federal Unemployment (FUTA) Tax Return and Adjustments.

Forms 941: Employer's Quarterly Federal Tax Return and Adjustments.

Forms 943: Employer's Annual Federal Tax Return for Agricultural Employees and Adjustments.

Yes, as a general rule, the IRS allows electronic filing for the current taxable year and prior 2 years. For Forms 941 and 941-X where the processing year is the same as the taxable year, forms can be efiled for 2 years going back, i.e. in 2026 you can file a form 941 for 2026, 2025 and 2024. For annual forms 940, 943, 944 and 945 and their corresponding adjustment forms, where the processing year is ahead of the taxable year, forms can be efiled for 3 years back, i.e. in 2026 you can file a form 940 for 2025, 2024 and 2023.

TaxMe processes electronic filings as quickly as possible. In most cases, IRS acknowledgments are emailed within 24 hours. However, same-day filing, same-day transmission, or timely IRS acceptance is not guaranteed when a return is submitted or paid near the filing deadline. Draining periods occur every 3 to 4 hours. IRS acknowledgments are emailed within 24 hours. This 24 hour window considers the potential impact from IRS regular scheduled system maintenance interruptions but does not consider "shutdown / cutover" periods.

The IRS systems have weekend maintenance windows lasting an average of 16 hours and major system upgrades that usually occur in the months of December and January. Every December through the first days in January of the following year, the IRS systems have "shutdown / cutover" periods causing IRS systems to be non-operational. These "shutdown / cutover" periods can last weeks and are used to prepare the IRS systems for the upcoming year filing season. During these periods, you can still submit your electronic returns. However, all returns will be queued and will not be transmitted until the IRS systems are fully operational.

Taxpayers should not wait until the last minute to submit a return or pay the TaxMe filing fee. Submitting a return, uploading information, or paying the filing fee near the end of the due date does not guarantee that the return will be transmitted to the IRS before the deadline.

Electronic filing depends on several factors, including payment completion, system processing, transmission timing, IRS availability, IRS maintenance windows, internet connectivity, and other technical conditions outside the taxpayer’s immediate control.

To help secure a timely filing, we recommend that taxpayers submit the return and complete payment at least 6 hours before the filing deadline. Returns submitted or paid after this recommended cutoff may still be processed, but TaxMe cannot guarantee that they will be transmitted or accepted by the IRS before the due date expires.

The taxpayer remains responsible for submitting the return and completing payment early enough to allow sufficient time for processing and transmission.

Immediately after a return or group of returns are transmitted to the IRS, an acknowledgment is received in our system. This acknowledgment, which comes in Extensible Markup Language format (xml), identifies each particular return and whether it has been accepted or rejected. If a particular return is rejected, the xml file will identify the reasons of the rejection for a particular return. The language used in these communications is based on predefined business rules established by the IRS.

TaxMe generates an email for each tax return submitted with a brief description of the result and an attachment in Adobe Acrobat format (pdf), which contains the interpretation of the xml file received from the IRS. To ensure that our emails don't end up in your spam folder, add info@tax-me.com to your contacts or list of safe senders.

If a return is accepted, the email confirmation will be simple to understand and no further action is needed from the taxpayer. However, if a return is rejected, the email communication will try to interpret the error and supply the taxpayer with the actions needed to correct the return.

Our policy gives taxpayers a 10 day window to correct an employment tax return (94x series) after the first rejection at no additional charge. The taxpayer will be ultimately responsible to meet our 10 day correction window.

If the taxpayer fails to submit a correction within a 10 day period after the first rejection, the return will be discarded from our systems and the taxpayer will have to submit a new return online and pay a new e-filing fee.

Once a return is electronically filed with the Internal Revenue Service, TaxMe will not issue a refund. Rejected employment tax returns within the 94x series can be corrected within our 10 day correction window at no additional cost to the taxpayer.

You are required to make employment Federal Tax Deposits (FTD's) based on the deposit schedule of your business, this could be monthly or semi-weekly. Before the beginning of each calendar year, you must determine which of the two deposit schedules you are required to use. To determine your payment schedule, review Publication 15.

Deposits for FUTA Tax (Form 940) are required for the quarter within which the tax due exceeds $500. The tax must be deposited by the end of the month following the end of the quarter.

If you fail to make a timely deposit, you may be subject to a failure-to-deposit penalty of up to 15%.

There are basically 5 options to make a Federal Tax Deposit:

EFTPS website (average registration period is 45 days): The Electronic Federal Tax Payment System (EFTPS) is provided free by the U.S. Department of the Treasury. After you've enrolled and received your credentials, you can pay any tax due to the Internal Revenue Service (IRS) using this system. You must be enrolled to use the EFTPS tax payment service. If enrolling for the first time, your information will need to be validated with the IRS. After validation is complete you will receive a personal identification number (PIN) via U.S. Mail in five to seven business days at your IRS address of record. Click here to enroll with EFPTS.

TaxMe's IRS Payments button (registration period takes only 2 hours): TaxMe is registered with the IRS to make federal tax payments on behalf of our clients. Enrollment is required for new clients and can take a few hours. Once enrollment is complete, TaxMe can process payments immediately. Clients will receive an "Inquiry PIN" which allows them to check payment history at EFTPS.gov or by phone. This Inquiry PIN will NOT give the taxpayer the ability to make or cancel payments.

Important: Payments must be scheduled by 6 p.m. ET the day before the settlement date to be received timely by the IRS. The funds will move out of your banking account on the date you select for settlement unless it falls on a weekend or a holiday. If the settlement date you choose falls on a weekend or a holiday, it will be changed to the next available business day.

How does our process work? Before you submit your payment request you will be able to download and review your payment details. Immediately after you submit your payment request, an alert will display on top of your screen and our system will send an email confirmation. TaxMe will charge a percentage fee over the amount of your payment request. Our fee will be billed separately. and must be paid before we can initiate a payment request. If you notice an error in your payment request after you paid our fee and our system began processing your request, you are responsible. Payment submissions that we receive without payment are discarded within 2 hours.

TaxMe's 94x return e-Filing (no registration required): When you e-file a return with TaxMe, you can pay taxes owed for an amount no greater than $2500.00 (941 or 944) or no greater than $500.00 (940). A percentage fee over the payment amount will be charged in addition to the regular e-filing fee.

Via other web services: The IRS uses third party payment processors for payments by debit and credit card. It's safe and secure; your information is used solely to process your payment. Click here for additional information.

By phone: You can always make a tax payment by calling the EFTPS voice response system at 1.800.555.3453. Follow the prompts to make your payment.

Remember, your tax payment is due regardless of the availability of any of these options.

If you pay independent contractors, you may have to file Forms 1099-NEC, Nonemployee Compensation, to report payments for services performed for your trade or business. If the following four conditions are met, you must generally report a payment as non-employee compensation (NEC), by January 31:

1. You made the payment to someone who is not your employee;

2. You made the payment for services in the course of your trade or business (including government agencies and nonprofit organizations);

3. You made the payment to an individual, partnership, estate, or in some cases, a corporation; and

4. You made payments to the payee of at least $600 during the year.

The January 31 deadline began as part of the Protecting Americans Against Tax Hikes (PATH) Act legislation to combat identity theft and refund fraud.

Penalties

Failure to file a correct information return by the due date (Sec. 6721):a) $50.00 per information return if you correctly file within 30 days. b) $100.00 per information return if you correctly file more than 30 days after the due date but before August 2. c) $270.00 per information return if you file after August 1. Certain exceptions apply.

Failure to furnish correct payee statements (Sec. 6722): If you fail to provide correct payee statements and you cannot show reasonable cause, you may be subject to this penalty. Penalty amounts are similar to those stated above. Certain exceptions apply.

If you made an error on Form 1099-NEC, box 1, of $100.00 or less, or in the tax withheld of $25.00 or less, then you may not need to correct a return based on the Safe Harbor rules for De Minimis Dollar Amount Errors on Information Returns and Payee Statements under sections 6721 and 6722. Click here for more information.

All our Excel files are spreadsheets with extensions ".xlsx". These files do not use any type of code (macros) and are designed to simplify e-filing of multiple (bulk) forms simultaneously.

You can use our excel files with Google Sheets or Miscrosoft Excel. Both are universally available and free.

If you reach a webpage with the option to prepare your information using a spreadsheet, simply download the file and save it in any location in your local machine. You can prepare the information at your convenience.

When you upload a file through one of our online products, our systems will perform a variety of checks to ensure your information is accurate and will alert you if any errors are found. All our web products are user friendly and are designed so users can explore and test the system free of charge. Only if you are fully satisfied and payment of our fee is made, then, we will electronically file your forms.

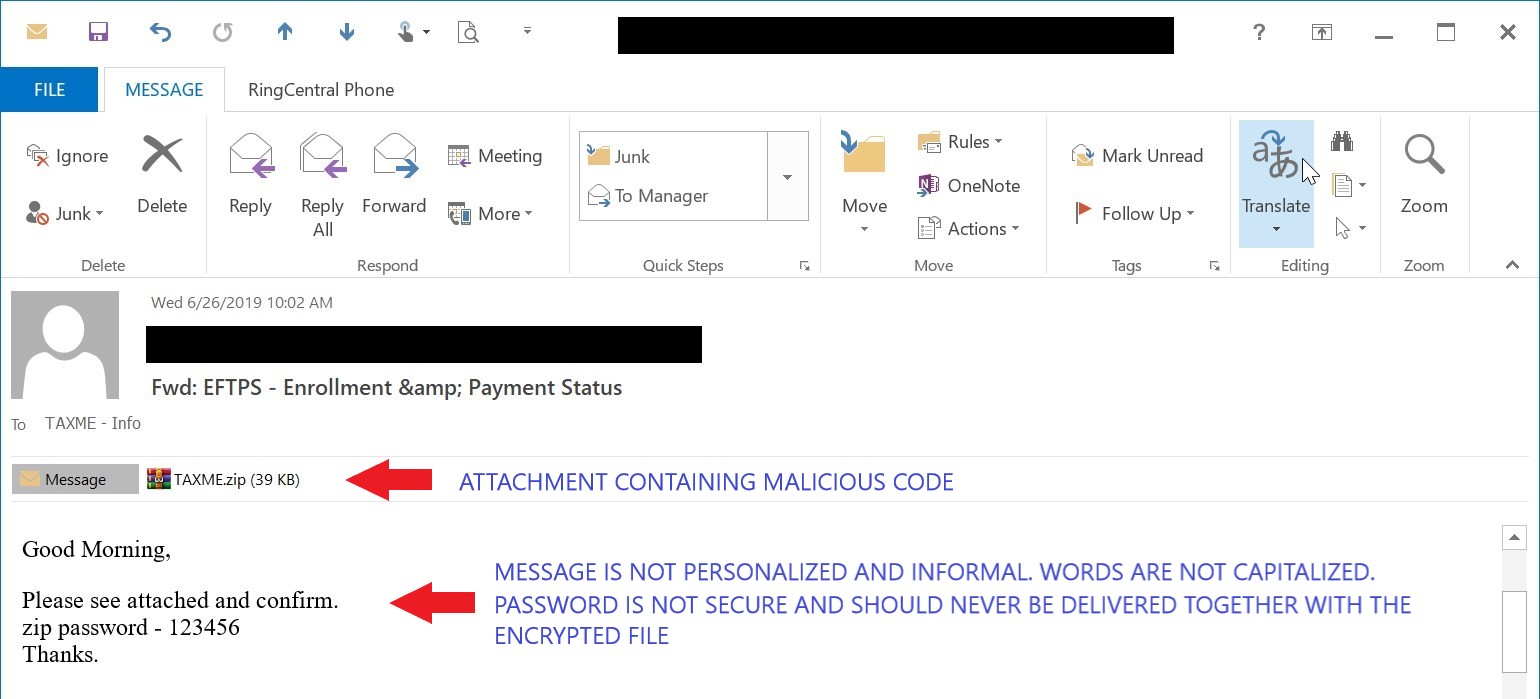

Phishing attacks use email or malicious websites to get personal information from the user. In many cases, the criminal fools someone into believing the phishing email is from someone they trust. The emails often have the look and feel of authentic communications. These targeted messages can trick even the most cautious person into doing something that may compromise data.

People should be vigilant and skeptical. Even if the email is from a known source, people should use caution because cybercrooks are very good at mimicking trusted businesses, friends and family.

If you receive an email claiming to be from TaxMe that contains a suspicious ".zip" attachment:

Don't reply.

Don't open any attachments. They can contain malicious code that may infect your computer or mobile phone.

Don't click on any links.

Forward - preferably with the full email headers - the email as-is to us at phishing@tax-me.com. Don't forward scanned images because this removes valuable information.

Delete the original email.

If you receive an email you suspect contains malicious code or a malicious attachment and you HAVE clicked on the link or downloaded the attachment.

Visit OnGuardOnline.gov to learn what to do if you suspect you have malware on your computer.

If you receive an email you suspect contains malicious code or a malicious attachment and you HAVE NOT clicked on the link or downloaded the attachment.

Forward the email to spam@uce.gov which is the Federal Trade Commission's email address for deceptive spam. Learn more at ftc.gov

Below is an example image of a suspicious email.

×

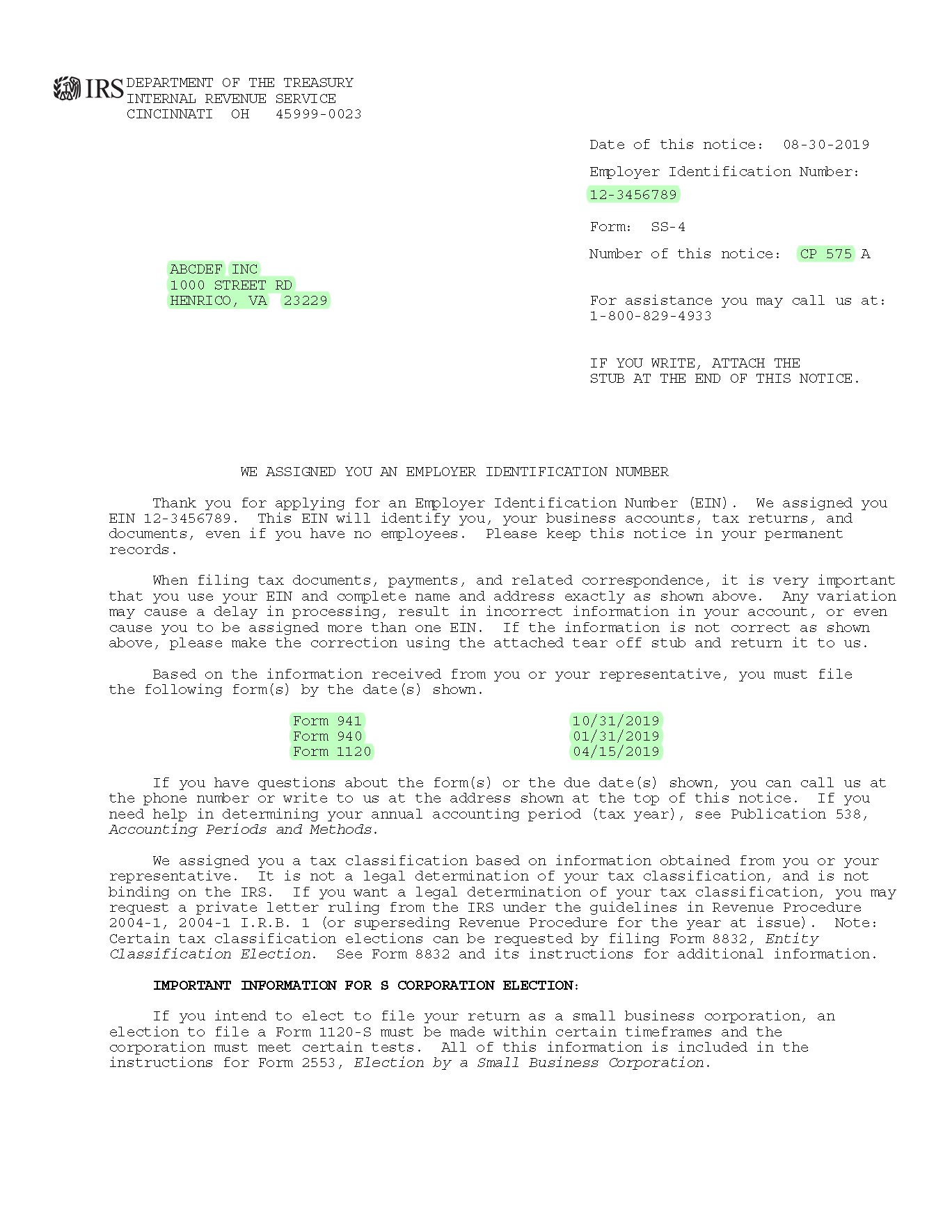

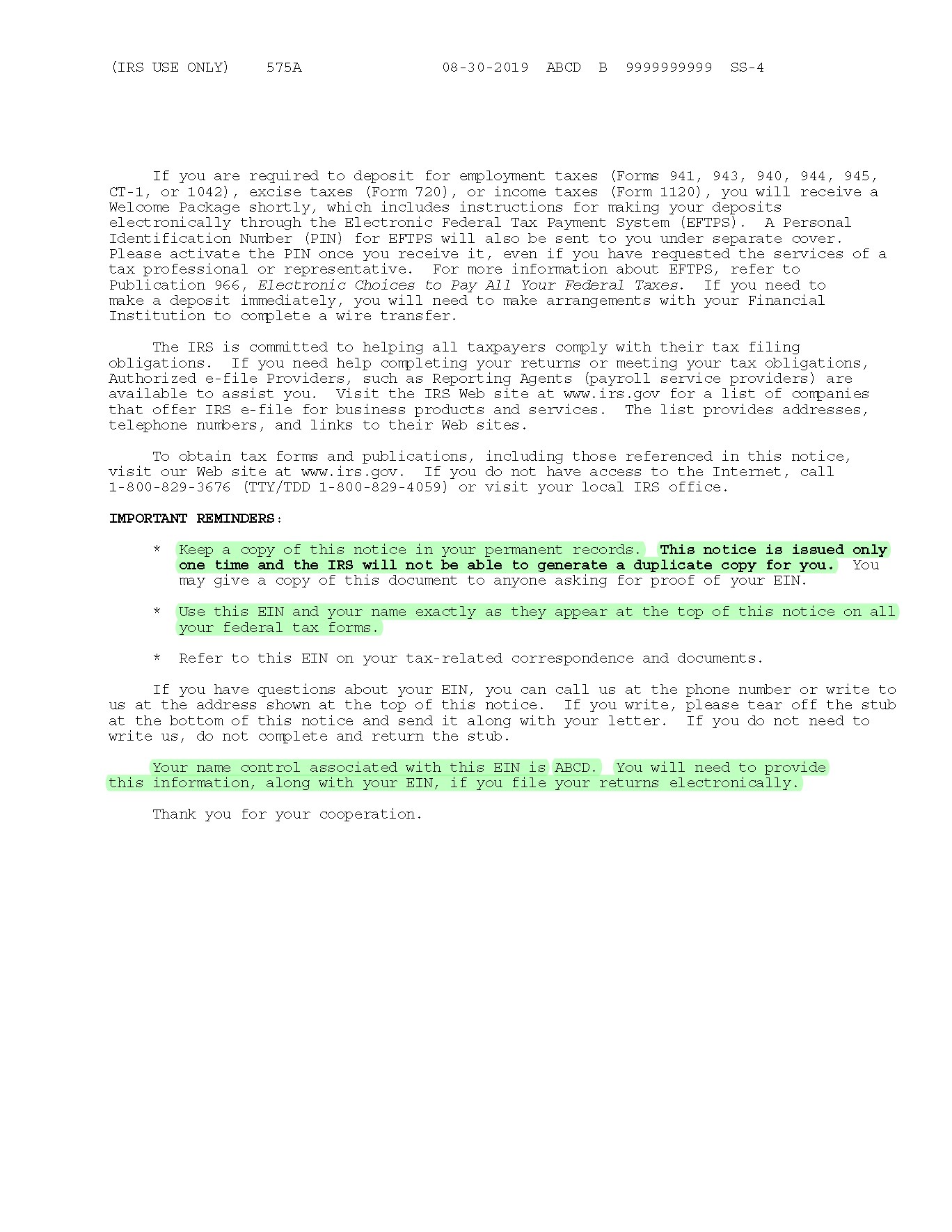

A business applying for an EIN is required to complete Form SS-4 (Application for Employer Identification Number).

Notice CP 575 is an IRS document generated when a business is assigned an EIN.

Below is a list of possible situations where your Notice CP 575 becomes handy:

When opening a new bank account, financial institutions will ask for proof of identification.

Differentiating between Business Name and Trade Name. Sometimes taxpayers confuse the two when e-filing a tax return which will cause it to be rejected.

All IRS correspondence will be delivered to the address shown on this notice.

Notice CP 575 lists the federal tax forms required to be filed and their corresponding deadlines.

NAME CONTROL. It generally results from the first 4 characters of the business name with certain variations (i.e. when the name of the business is too short or has special characters). When a federal return is e-filed, the IRS will match the name control against the EIN. If no match is found it will reject the return.

The images below show a sample CP 575 highlighted with some of the items listed above.

×

If a browser is configured to a foreign language other than English, or if a user is located in a foreign country, users can experience unexpected behavior when entering values on our web forms. Depending on your browser's geographical location settings, number values may be interpreted in different formats.

Our systems are designed to process number formats in US(1,000.00). However, a machine located in Germany or set to use German as the default language, will interpret numbers as DE(1.000,00). Notice the difference in the thousand and decimal separator. This will generate calculation errors.

To fix this issue, follow these steps (other browsers may have different settings menus):

In Chrome click the top right menu (three vertical dots) and select Settings

Scroll down and expand the Advanced option

Under Languages click the drop down arrow next to Language

If English is not listed under Other languages based on your preference, click Add languages and add English as a new language

Click the three vertical dots next to English and check the box Display Google Chrome in this language

Restart Chrome browser. All numbers entered in our forms will be interpreted in the correct format.

These two forms are not interchangeable. The employer should never flip-flop between the two forms on their own and should always file according to their designated filing requirement, which are set by the IRS when applying for an EIN on Notice CP 575

If you're currently required to file Form 944, Employer's Annual Federal Tax Return, but estimate your tax liability to be more than $1,000, you may be eligible to update your filing requirement to Form 941.

If you're an employer required to file a Form 941 but estimate your tax liability will be $1,000 or less for the tax year, you may be eligible to switch to Form 944.

To request a change, you must send a written request, postmarked by March 15 of the current year or call the IRS by April 1 of the current year. The IRS will send a written notice if it changes your filing requirement.

Form 941, Employer's Quarterly Federal Tax Return. This form allows employers to report employment tax liabilities each quarter. Employers use Form 941 to report income taxes, Social Security tax, Medicare tax and additional Medicare tax withheld from employee's wages, tips and other compensation, claim employment tax credits and adjustments, report the amount of employment taxes owed or claim an overpayment of employment taxes. If the IRS advises the employer to file Form 941 quarterly, they must do so.

Form 944, Employer's Annual Federal Tax Return. This form allows employers to report employment tax liabilities once a year, instead of quarterly and must be filed when employers owe $1,000 or less of employment taxes per year. This form can’t be used unless an employer receives official IRS notification that they are eligilble to use this form. Once the employer receives notice they can file Form 944, they must file this form every year. They must continue to file Form 944, regardless of the tax they owe, unless the IRS notifies them differently.

When you discover an error on a previously filed Form 94x series, you must correct it using Form 941-X, 943-X, 945X or by checking the Amended box of Form 940

Form 941-X: Do not file Form 941-X to correct the number of employees or to adjust federal tax deposits.

Generally, Form 941-X must be filed within 3 years starting April 15 of the following year of the year of the return. For example, if you are amending any quarter of a 2025 Form 941, you can file Form 941-X by April 15, 2029. In this example, the IRS starts the clock on April 15, 2026. This is called "period of limitations".

Also, if you are correcting overreported amounts and are filing form 941-X in the last 90 days of a period of limitations, you MUST use the claim process. You can’t use the adjustment process. If you’re also correcting underreported amounts, you must file another Form 941-X to correct the underreported amounts using the adjustment process and pay any tax due.

We recommended you read the instructions carefully before completing your adjustments. Key items to be familiar are whether you underreported or overreported wages and whether you want to claim a refund or want to apply a credit to a future form 941.

Form 940: To amend or make a change to an already filed Form 940, check the Amended box in the top right corner of Form 940, fill in all the amounts that should have been on the original form, an explanation is required and available within the form.